In addition to the balance sheet, the income statement — also known as the profit and loss statement abroad — is one of the most important analyses of double accounting. But how is an income statement correctly prepared and interpreted in accordance with Swiss Code of Obligations (OR)?

What is an income statement?

The income statement shows the expenses and income of a company over a specific period of time. The difference between expenses and income results in profit or loss.

Note: Income statement is the common term in Switzerland, while abroad it is often referred to as profit and loss statement (P&L). However, it is the same thing.

Difference between balance sheet and income statement

The balance sheet and income statement are the two most important evaluations of double accounting:

- Die balance sheet shows assets and liabilities at a specific point in time.

- Die income statement shows expenses and income over a specific period of time.

Both evaluations show the company's profit or loss, which must match for the accounting to be accurate.

The balance sheet therefore provides a snapshot at the end of a specific period of time, usually at the end of the year. The income statement, on the other hand, is like a movie, which shows the company's performance over a specific period of time, usually over a fiscal year.

Structure of an income statement

The income statement is a list of expense and income accounts, divided into standardized subgroups and subtotals.

Requirements for an income statement in accordance with OR

The following requirements are in accordance with Art. 959b OR and the principles of proper accounting in accordance with Article 958 OR comply with:

- Clear structure and order: The positions must be presented in the order prescribed by law.

- Individual designation of positions: In principle, items may not be offset against each other (gross principle).

- Recurring periods: Income and expenses must be correctly allocated to the corresponding period (e.g., down payments for work not yet done or expenses already paid, the payment of which only accrues in the following year, must be accrued).

- Additional disclosure: If significant for third parties, further items must be listed separately in the income statement or in the notes. Personnel expenses and depreciation/value adjustments must also be shown in the notes to the income statement in particular.

Structure of the income statement

An income statement using the total cost method (a so-called “production income statement”), which is common in Swiss SMEs, must be structured as follows:

- Net revenue from supplies and services

- Inventory changes in unfinished and finished products and uninvoiced services

- Cost of materials

- personnel expenses

- other operating expenses

- Depreciation and value adjustments on fixed asset positions

- Financial expenses and income

- non-operating expenses and non-operating income

- extraordinary, one-time or non-period expenses and income

- direct taxes

- Annual profit or loss

Do I have to list every position?

Items in the income statement that have no or only an insignificant value must, in accordance with Item 958d OR not necessarily be listed separately.

Single-stage vs. multi-level income statement

In Swiss accounting, there are basically two types of income statement: the single-level income statement and the multi-level income statement.

While the single-level income statement is suitable for a quick overview, the multi-level variant allows a deeper and more precise analysis of business results.

Single-level income statement

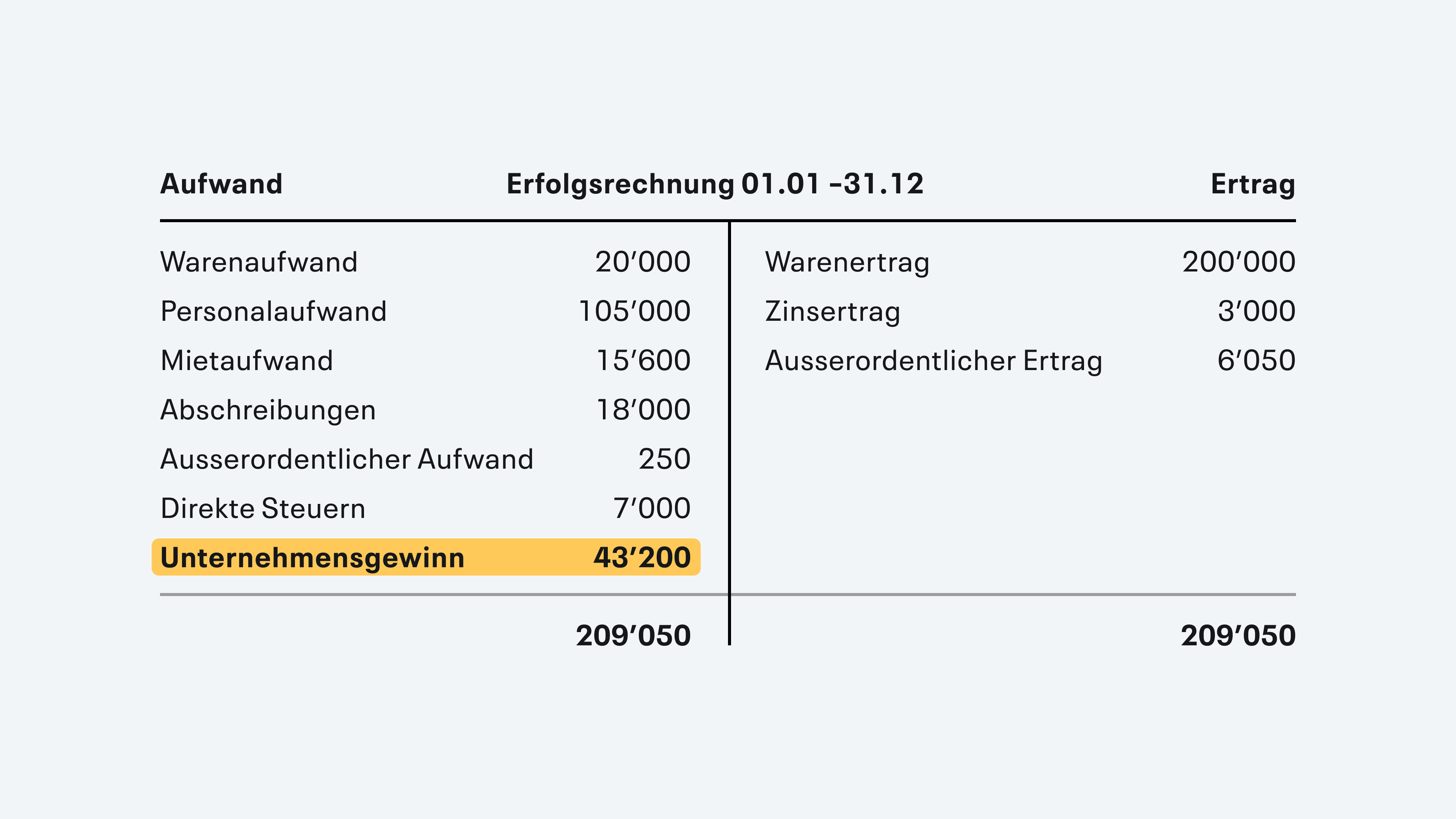

The single-stage income statement is the simplest form of profit calculation. In doing so, all income is added up and all expenses are deducted from it. The result is profit or loss. This variant provides a quick overview, but little detailed information about the origin of the profit.

Multi-level income statement

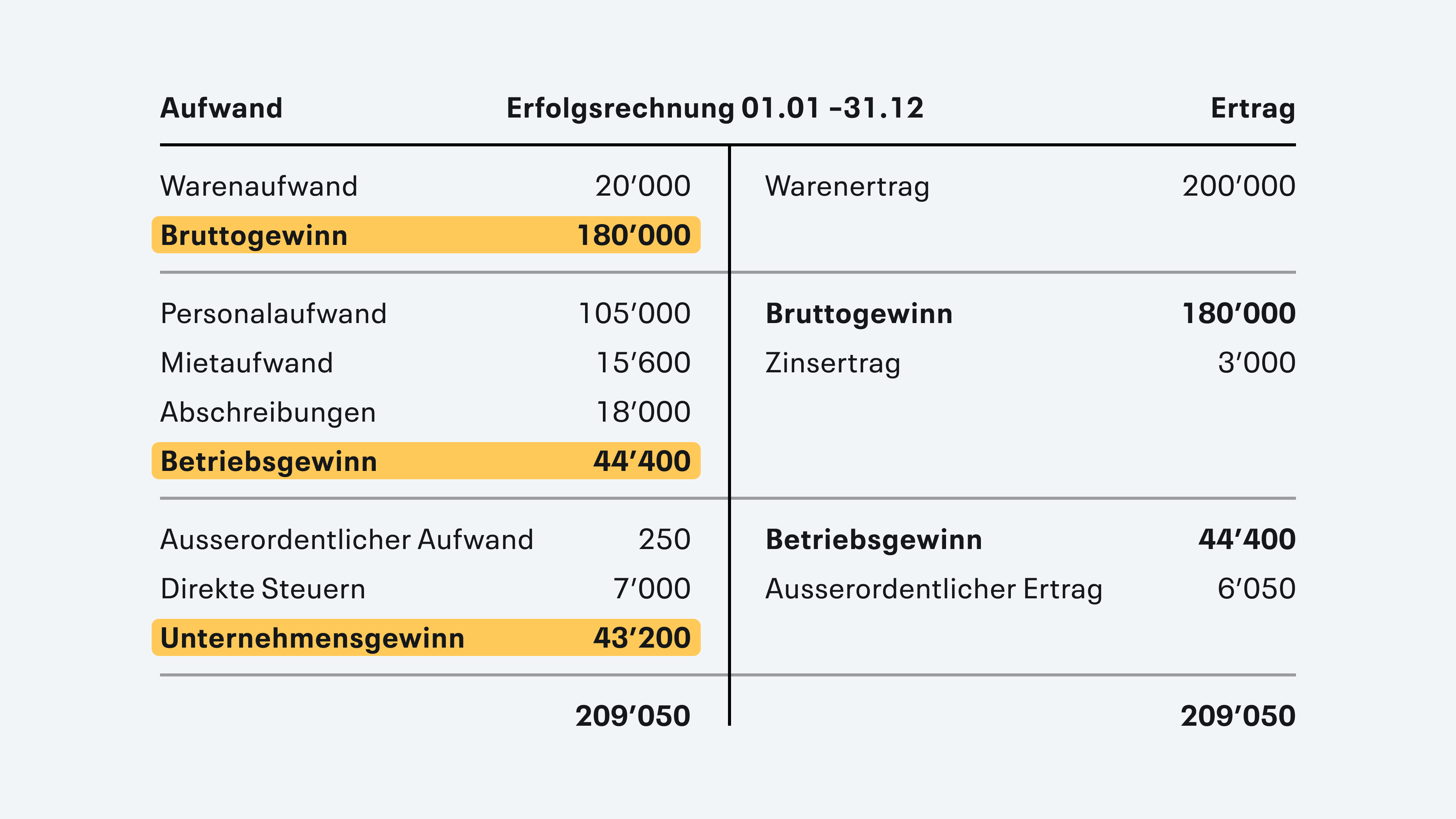

In contrast, the multi-level income statement divides success into several steps. This creates a more detailed picture of a company's economic situation:

- Gross profit: Sales (income) minus direct costs (such as cost of goods)

- Operating profit (EBIT): Gross profit minus operating expenses (e.g. personnel, rent, marketing)

- Corporate profit: Operating profit minus non-operating expenses and income (such as interest, real estate income or taxes)

The multi-level income statement offers more transparency and makes it possible to specifically identify weak points and strengths. This provides companies with valuable information to optimize their operating results.

Expenditure types and income types

There are various categories of expenses and income that you should consider. You can sign up for the outline on SME chart of accounts orient. In Swiss accounting software The structure of this chart of accounts is automatically stored.

Main types of expenses

- Cost of materials: These expenses relate to the purchase of raw, auxiliary and operating materials necessary for production.

- Personnel expenses: This includes the salaries and wages of employees as well as all associated social benefits.

- Depreciation: Depreciation records the loss in value of fixed assets, such as machinery or buildings, over their useful life.

- Operating expenses: This includes all operating costs, such as rent, energy costs and insurance.

Overview of income types

- Operating income: This category includes all income generated by the main business activity, such as selling products or services.

- Interest income: Income from interest received by the company through investments or loans.

- Other income: This section may include any other income that is not directly related to main business activities, such as one-off sales of fixed assets.

How to read an income statement

By reading the income statement, you get an overview of the company's income and expenses and can draw conclusions about the profitability and efficiency of business activities.

- At the top of the income statement, you will find the turnover that the company achieved in the period.

- Costs such as material costs, wages and other operating costs are then deducted from this. Here you can therefore read how high the expenses are.

- Using the “Gross Profit”, “Operating Profit (EBIT)” and “EBITDA” subtotals, you can identify the profitability of operating business and compare it over periods.

- At the end of the income statement, you will find the net profit or loss for the period.

Another relevant point is the comparison with previous periods or industry figures. This can help to objectively evaluate the company's performance.

Special eye marrow should also be placed in unusual positions, as they can influence the result but do not have to occur regularly in the future.

How do I create an income statement?

Step-by-step guide

Here we will guide you through the essential steps to create a successful and error-free income statement.

- Start by recording all relevant documents: Collect all receipts and documents relating to income and expenses. This includes invoices, receipts, bank statements, and contracts. Any document can be decisive, so don't leave anything out.

- Categorize your income and expenses: Allocate income and expenses to their respective categories. Each item should be correctly assigned to avoid subsequent corrections.

- Determine the turnover: Add up all sales and other income to determine total revenue. This sum is decisive for further calculations, so make sure you don't miss any income.

- Determine the total costs: Add up all expenses necessary to generate sales. This includes material costs, wages, rents, and other operating expenses. Accurate recording ensures precise results.

- Calculate gross profit: Subtract total costs from income to calculate gross profit. This key figure shows you how profitable your business is at first glance.

- Include depreciation and interest: Make a list of all other operating income and expenses, such as depreciation or interest, in order to arrive at operating income.

- Create the final layout of the income statement: Put all collected information in a clear and comprehensible form.

- Audit and control: Finally, check all information carefully for accuracy and completeness. It is particularly suitable here to compare with the balance sheet to see whether the profit or loss matches.

Accounting software for income statement

Modern accounting software creates your income statement automatically and without errors. With infinity.swiss You not only receive a simple income statement, but a detailed multi-level presentation that gives you valuable insights into your company's performance.

Benefits of an automated income statement:

- saving time: No need for manual calculations anymore

- Mitigate errors: Automatic booking reduces calculation errors

- Always available: Retrieve the current income statement at the click of a mouse

- Swiss compliance: Automatic compliance with OR regulations

- Comparison options: Easy comparison between different periods

With infinity.swiss, you can have a current income statement prepared for any period and download it directly as a PDF — ideal for interim financial statements or spontaneous evaluations.

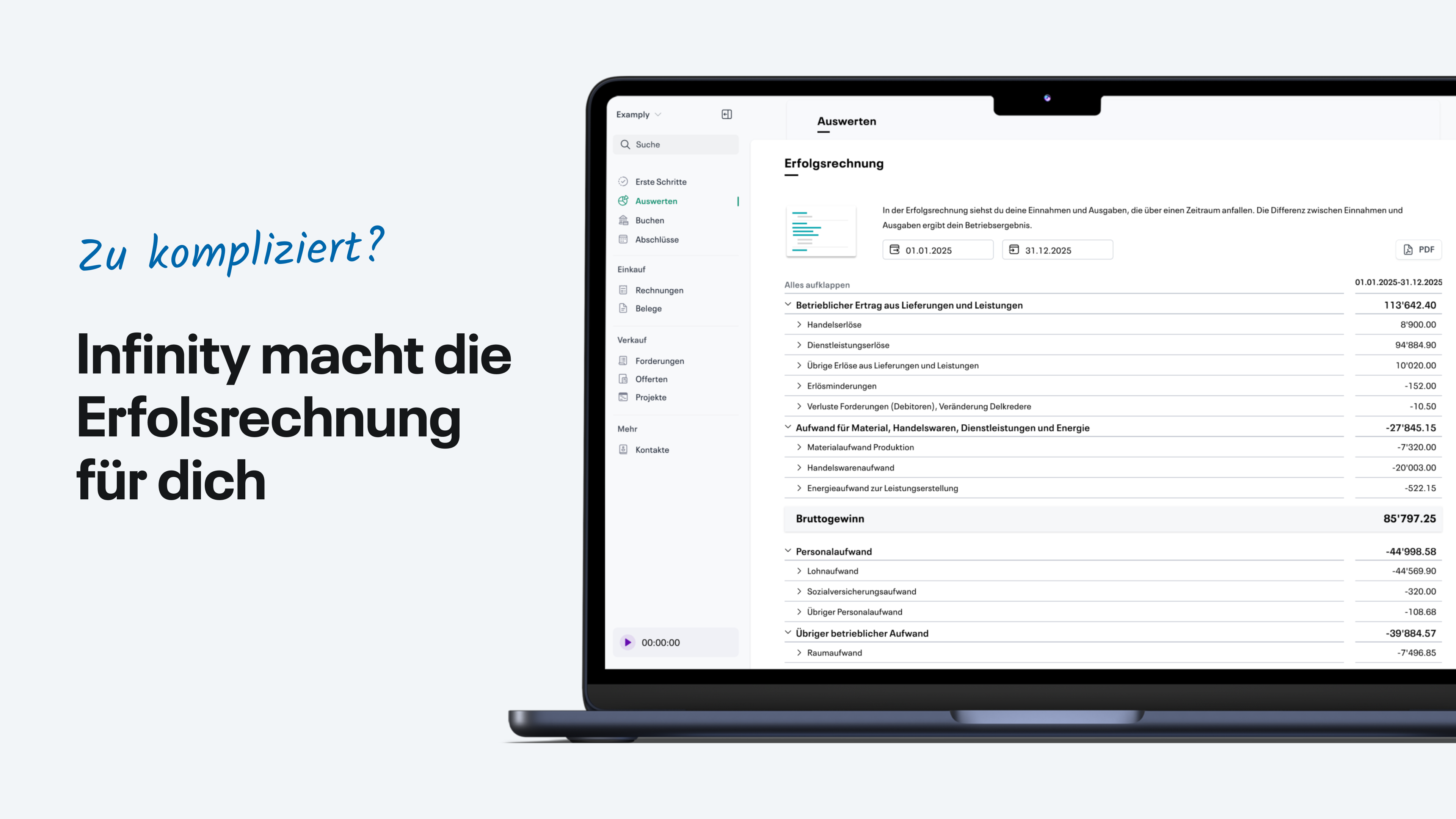

This is what an income statement looks like in infinity.swiss

The screenshot shows the user-friendly infinity.swiss interface displaying a multi-level income statement. Here you can see all important elements at a glance:

- Flexible periods: You can use the date fields to select any period — from monthly financial statements to annual financial statements

- Multi-level construction: The income statement shows the path from sales to gross profit and EBITDA to net profit in a clearly structured manner

- Openable positions: Each main category can be opened as needed to view detailed bookings

- Instant PDF export: By clicking on “PDF”, you will receive a professionally formatted income statement for authorities or business partners

- Automatic calculation: All subtotals and key figures are calculated automatically — calculation errors are a thing of the past

Particularly practical: You can retrieve the income statement at any time and don't have to wait until the end of the year. This allows you to keep track of your company's development throughout the year.

Three practical examples from various industries

Freelancer agency without warehouse: For service companies, material costs are usually low — the focus is on personnel costs and operating expenses. Here you can measure operational efficiency particularly well, as the EBITDA margin often exceeds 30%.

E-commerce store: Goods and shipping costs dominate the cost structure. Inventory changes have a direct effect on gross profit and must be recorded cleanly. The gross profit margin is a key figure for success here.

SaaS startup: Material costs play a minor role, but development costs and marketing are usually high. It is important to differentiate between EBITDA and actual cash flow, as these can differ significantly from one another.

These examples show how different income statements can look depending on the sector. With modern accounting software such as infinity.swiss You automatically receive the relevant key figures for your industry and can optimally monitor your performance.

Key figures of the income statement

turnover

Sales include all income a company receives from the sale of goods and services within a specific period of time. It forms the starting point of the income statement.

gross profit

The gross profit is derived from sales minus direct manufacturing costs (costs of goods and materials). It shows the profitability of the core business without taking into account fixed costs such as rent, IT expenses, wages, etc.

Operating profit (EBITDA)

EBITDA (earnings before interest, taxes, depreciation and amortization) measures operating profit before interest, taxes, depreciation of tangible assets and intangible assets. It makes it possible to compare profitability between companies in different industries and investment levels.

Amortization vs. amortization in EBITDA

note: The English word “amortization” in the EBITDA abbreviation here means depreciation of intangible assets and has nothing to do with the frequently confused German term “amortization,” which describes a repayment of a financial debt.

EBIT

EBIT (earnings before interest and taxes) measures operating profit after depreciation and amortization, but with Interest and taxes. It is a key indicator of a company's operational performance and profitability.

net profit

Net profit (or net loss if negative), often referred to as net income, is the final result that remains after deducting all expenses, costs, and taxes from a company's income.

In double accounting, the net profit on the income statement must match that from the balance sheet — otherwise an error has been made in the accounting department.

Frequently asked questions about income statement

Do I have to prepare an income statement?

According to Swiss Code of Obligations (OR), the following companies must prepare an income statement:

- Joint stock companies (AG)

- Limited liability companies (GmbH)

- cooperatives

- Sole proprietorships or collective companies that have an annual turnover of over CHF 500,000

Even for sole proprietorships below the threshold, it can be worthwhile to conduct proper double accounting for better evaluations, simpler VAT settlement and more security in tax statements.

With dual accounting software such as infinity.swiss, an income statement can then be created automatically with just one click, even without previous knowledge.

When does an income statement have to be prepared?

An income statement should ideally be prepared once a year at the end of the fiscal year.

Ideally, you should also check the current status of expenses and income more frequently during the year — automated accounting software is suitable here so that an income statement can be retrieved at any time with a click.

For which period is the income statement prepared?

The income statement is usually prepared for a full financial year.

In accounting software, however, an income statement for any other period, such as a specific quarter, can also be created with just a few clicks. This can be helpful, for example, when comparing seasonal sales quarters.

What happens if my income statement is negative?

A negative result in the income statement means that expenses exceed income, resulting in a loss.

If you have a net loss in the income statement, you must do so at the end of the financial year with your equity above the “Annual Profit and Loss” account Calculate.

However, especially with startups and young companies, it is often the case that no positive result is achieved in the first few years — such losses can then be offset for tax purposes for 7 years. In the long term, however, losses must not be ignored, even with good liquidity, so that the company remains viable.